Wool prices surge — now what?

By Chris Wilcox

Chairman of Poimena Analysis

Chairman of the International Wool Textile Organisation’s Market Intelligence Committee

After a steady and moderate rise between September 2014 and early April 2015, wool prices have surged since Easter. In some cases, wool prices have reached record levels in nominal terms. No doubt this has led sheep producers to ask what is driving these higher prices and how long the price rise will last. An equally, if not more important question, at least for long term planning, is whether global demand can be sustained at levels which encourage producers to stick with wool in their enterprise.

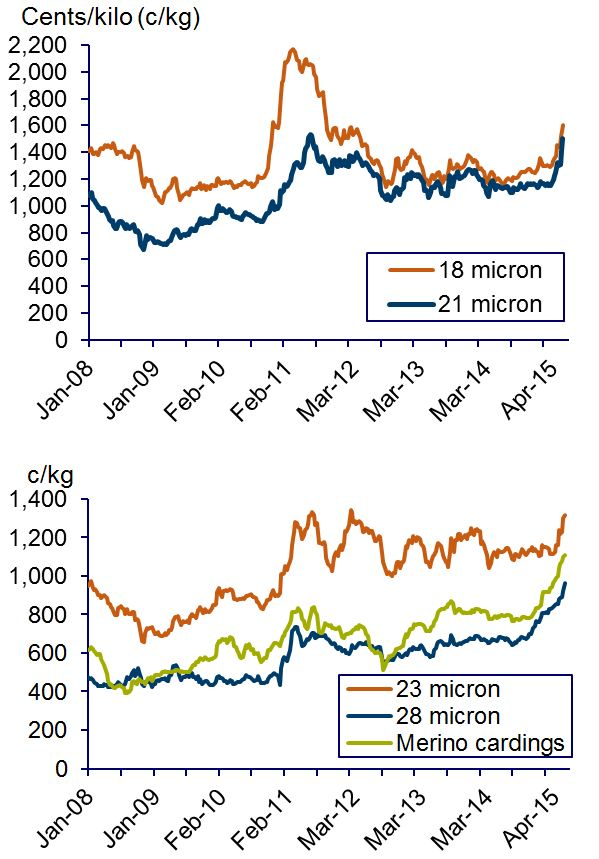

Before we look at these questions, let’s recap what has happened to wool prices. Figure 1 shows the trends in some selected wool price guides since January 2008. The surge in prices in the past couple of months can be seen for all of these price guides, but is particularly marked for cross-bred wool (28 micron) and for Merino cardings. These prices have been rising steadily since October 2014 and for both of these (and other cross-bred price guides) the current levels (as at 5 June) are the highest ever recorded.

Prices for Merino fleece wool (23 micron and finer) have also increased, albeit at a lesser rate, and have only recently seen a sharp rise. Some welcome news for superfine woolgrowers is that prices for superfine wool (18.5 micron and finer) have lifted steadily since October, although prices are only back to levels seen in early 2012, and well short of the heights reached in 2011.

So, what’s behind the recent leap in wool prices? And, why are prices for cross-bred wool and cardings at such high levels?

Fall in the Australian dollar (A$)

One factor behind the lift in wool prices over the past six months has been has been an appreciation of the United States dollar (US$) against most currencies, including the A$. After being above 90 US cents for most of the four years between September 2010 and September 2014, the A$ fell to 76.6 US cents at the end of May, a 19% depreciation from the end of September. This has encouraged increased demand for wool. In spite of the increase in wool prices in A$ terms, wool prices in US$ have only increased by a modest 5% or so. For mills in China, current US$ prices for most wools are still below the levels seen as recently as October 2013.

Better business conditions in the wool textile industry

While the drop in the A$ has helped, the main reason for the increased auction demand and prices has been better business conditions in the wool textile industry, most notably in China. The latest results from the International Wool Textile Organisation’s (IWTO) annual survey of the global wool textile industry shows that activity levels in the spinning, knitting and weaving sectors are well above normal levels and are expected to remain that way over the next few months. The early stage processing industry is seeing around normal activity levels. This is better than a year ago and activity levels are expected to lift over the next few months.

As well as the improved production activity levels, stocks within the industry of raw wool and semi-processed wool products have been run-down over the past 12 months and, in some cases, are below comfortable levels. This means that mills are increasing their purchases in part to replenish depleted stocks.

These positive conditions were reflected in an upbeat mood at the recent IWTO Congress in China. The woollen sector which uses shorter and often broader wools to make jumpers, tweed coats and overcoats is exceptionally strong, particularly in China. Demand from retailers and garment makers is very strong for woollen woven and knitted fabric, principally for women’s coats for the coming autumn/winter. A considerable portion of these coats are destined for the domestic China market, but the export market to Japan, Korea and the European Union (EU) is also strong.

Improving, but patchy, economic conditions and outlook

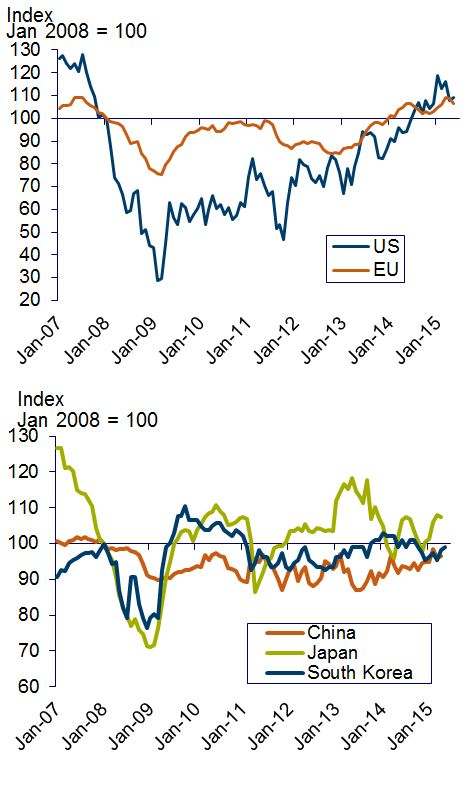

The improvement in business conditions in the wool textile industry has no doubt been aided by better economic conditions and outlook for the major advanced economies, notably in Europe. As a result, consumer confidence in the European Union and in the US has lifted to seven year highs recently. Consumer confidence is a little more mixed in Asia. Figure 2 shows the trends in consumer confidence.

With the better consumer confidence in key countries, prospects for better retail sales in autumn/winter 2015 in the northern hemisphere are improving, potentially boosting retailer orders in preparation for the autumn/winter.

Wool auction supply increases in the short-term, but could fall in 2015/16

Even though wool production in 2014/15 is predicted to be the same as in 2013/14, the higher auction prices have flushed wool onto the market. The Australian Wool Exchange (AWEX) reports that the weight of auction offerings to 5 June were up by 8%, while the Australian Wool Testing Authority (AWTA) reports a 1.9% increase in the volume of wool tested for the season to May. This increased supply has come from stock held in broker’s stores and, to a lesser extent, from on-farm stocks held over from previous seasons.

While supplies are up in the short-term, it is likely that supply will fall in 2015/16. The Australian Wool Production Forecasting Committee predicts that Australian wool production will fall by 2.7% in 2015/16 due to a lower national sheep flock. This, plus a low carry-over of stocks in to the new season, will mean that auction supplies are likely to be tight in 2015/16, particularly in the first couple of months.

Outlook for the first half of 2015/16

It seems that conditions are right for a continued cyclical upturn in wool prices, at least for the first half of the 2015/16 season. Economic growth forecasts in the major advanced economies are for an improvement in 2015 and 2016. While economic growth is slowing in China as its economy undergoes a necessary structural change, it is still expected to grow at a solid rate of a little under 7% per year in 2015 and 2016.

Business conditions in the wool textile industry are expected to be good at least for the first six months of 2015/16. The woollen sector could reach a peak in the next few months, and as a result, demand for broader wools and Merino cardings pulls back from the current high levels. However, the worsted sector (which uses a longer length fleece wool to produce a smoother fabric such as men’s suits) seems set for a good period of growth, which should help Merino fleece wools. The expected lower supply levels will also help support prices.

Of course, there are risks to this positive outlook. The global economy remains volatile and fragile, which could spell danger. For example, certain economies in Europe could still turn for the worse, which could put pressure on retail sales and orders through the wool textile pipeline, ultimately affecting raw wool demand.

A second issue is that of prices of competing fibres. These are relatively subdued and have not experienced much of an increase in the past six months. This is in contrast to 2011 when prices for all textile fibres surged, driven higher by a spike in cotton prices due to short-term shortages. Now, cotton stocks are at exceedingly high levels, holding back prices for both cotton and synthetic fibre. This could in turn dampen the extent of price increases for wool in US$.

Producers would also be well aware that there can be a correction following the kind of price surge we have seen in the past few weeks. This has happened in the past and is likely to happen again.

Longer term drivers for the wool industry

While the prospects over the next six months are relatively bright, what about in the longer term?

Based on my own analysis and assessment, the longer-term prospects for demand for Australian wool will hinge mostly on global economic conditions and consumer income growth. Less important will be the relative production volumes and prices of competing fibres such as cotton, polyester staple fibre, acrylic fibre and viscose fibre. Australian and world wool production volumes are unlikely to increase much, if at all. Meanwhile, world production of chemical and man-made fibres will continue to grow. Therefore, wool cannot compete on price. It must compete on value and the fibre qualities.

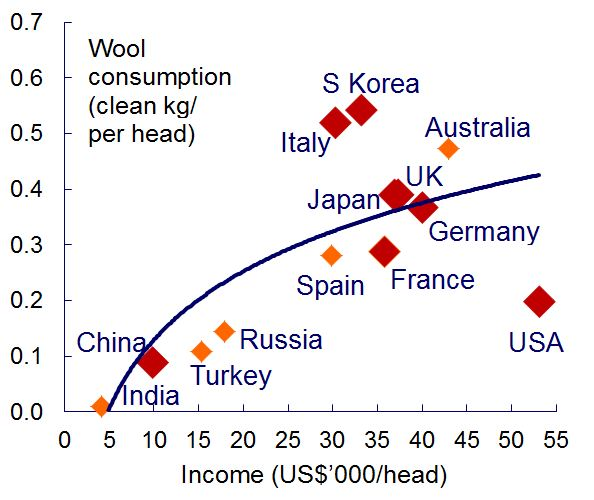

This will mean that wool clothing will appeal most to higher income consumers. As shown in Figure 3, there is a strong relationship between per capita income and the per capita consumption of apparel wool. The seven largest wool consuming countries in retail are shown by the large red markers. Wool consumption per capita in Australia is high, but with a relatively small population, total wool consumption in Australia is well below that of the seven largest consuming countries. The opportunities for growth in demand for wool are typified by the potential for per capita growth in China, Russia, India and Turkey.

With incomes being the most important driver, the key to growing demand will be products which meet consumer requirements and clothing trends. Worsted men’s suits, jackets and trousers, together with wool knitwear and women’s overcoats, will remain the backbone of demand for Australian wool. While there are likely to be fashion-driven fluctuations from year to year in the importance of these, as there currently is for women’s coats, the potential for longer-term growth in demand for wool will come from increased demand for active leisurewear (next-to-skin wear) and casual garments.

These product categories (both the traditional backbone categories and the potential growth categories) will determine the type of wool that will be demanded. It is therefore important for producers to understand the raw wool requirements that are used in each of these product categories.

While there will be sustained demand for wool in the longer-term, producers cannot simply rely on the hope that wool prices will increase. As indicated in the earlier discussion about the drivers in the current market environment, there are many external factors that influence wool prices and so prices will fluctuate. Producers should therefore develop a long-term strategy for their business that addresses the long-term opportunities that will be available and secures their long-term profitability.

Chris Wilcox is a key speaker at DAFWA’s Regional Sheep Updates on 28, 29 and 30 July 2015 and will cover this topic in more detail.