Wool prices surge — now what?

By Chris Wilcox

Chairman of Poimena Analysis

Chairman of the International Wool Textile Organisation’s Market Intelligence Committee

After a steady and moderate rise between September 2014 and early April 2015, wool prices have surged since Easter. In some cases, wool prices have reached record levels in nominal terms. No doubt this has led sheep producers to ask what is driving these higher prices and how long the price rise will last. An equally, if not more important question, at least for long term planning, is whether global demand can be sustained at levels which encourage producers to stick with wool in their enterprise.

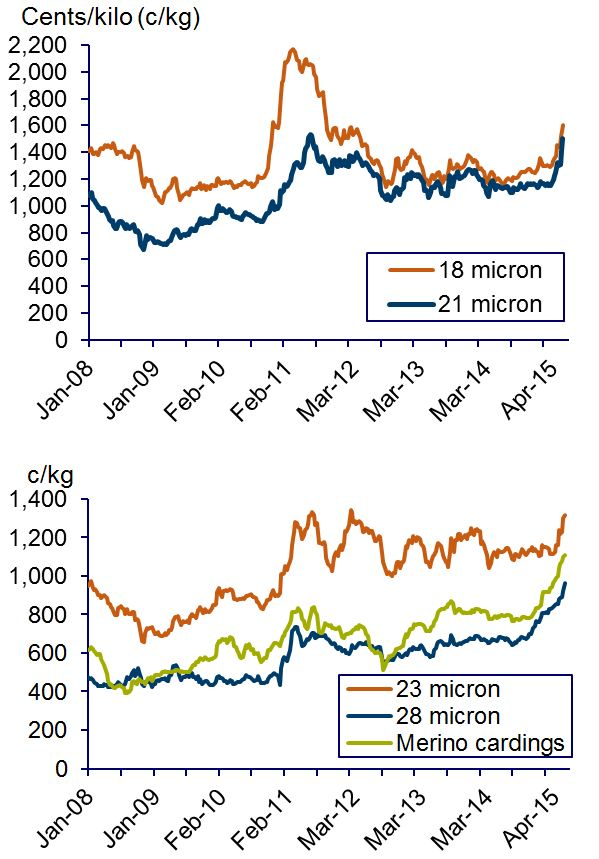

Before we look at these questions, let’s recap what has happened to wool prices. Figure 1 shows the trends in some selected wool price guides since January 2008. The surge in prices in the past couple of months can be seen for all of these price guides, but is particularly marked for cross-bred wool (28 micron) and for Merino cardings. These prices have been rising steadily since October 2014 and for both of these (and other cross-bred price guides) the current levels (as at 5 June) are the highest ever recorded.

Prices for Merino fleece wool (23 micron and finer) have also increased, albeit at a lesser rate, and have only recently seen a sharp rise. Some welcome news for superfine woolgrowers is that prices for superfine wool (18.5 micron and finer) have lifted steadily since October, although prices are only back to levels seen in early 2012, and well short of the heights reached in 2011.

So, what’s behind the recent leap in wool prices? And, why are prices for cross-bred wool and cardings at such high levels?

Fall in the Australian dollar (A$)

One factor behind the lift in wool prices over the past six months has been has been an appreciation of the United States dollar (US$) against most currencies, including the A$. After being above 90 US cents for most of the four years between September 2010 and September 2014, the A$ fell to 76.6 US cents at the end of May, a 19% depreciation from the end of September. This has encouraged increased demand for wool. In spite of the increase in wool prices in A$ terms, wool prices in US$ have only increased by a modest 5% or so. For mills in China, current US$ prices for most wools are still below the levels seen as recently as October 2013.

Better business conditions in the wool textile industry

While the drop in the A$ has helped, the main reason for the increased auction demand and prices has been better business conditions in the wool textile industry, most notably in China. The latest results from the International Wool Textile Organisation’s (IWTO) annual survey of the global wool textile industry shows that activity levels in the spinning, knitting and weaving sectors are well above normal levels and are expected to remain that way over the next few months. The early stage processing industry is seeing around normal activity levels. This is better than a year ago and activity levels are expected to lift over the next few months.

As well as the improved production activity levels, stocks within the industry of raw wool and semi-processed wool products have been run-down over the past 12 months and, in some cases, are below comfortable levels. This means that mills are increasing their purchases in part to replenish depleted stocks.

These positive conditions were reflected in an upbeat mood at the recent IWTO Congress in China. The woollen sector which uses shorter and often broader wools to make jumpers, tweed coats and overcoats is exceptionally strong, particularly in China. Demand from retailers and garment makers is very strong for woollen woven and knitted fabric, principally for women’s coats for the coming autumn/winter. A considerable portion of these coats are destined for the domestic China market, but the export market to Japan, Korea and the European Union (EU) is also strong.

Improving, but patchy, economic conditions and outlook

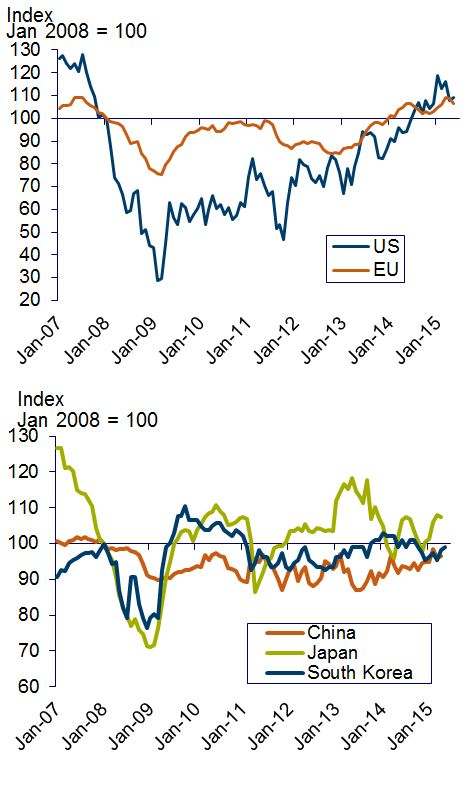

The improvement in business conditions in the wool textile industry has no doubt been aided by better economic conditions and outlook for the major advanced economies, notably in Europe. As a result, consumer confidence in the European Union and in the US has lifted to seven year highs recently. Consumer confidence is a little more mixed in Asia. Figure 2 shows the trends in consumer confidence.

With the better consumer confidence in key countries, prospects for better retail sales in autumn/winter 2015 in the northern hemisphere are improving, potentially boosting retailer orders in preparation for the autumn/winter.

Wool auction supply increases in the short-term, but could fall in 2015/16

Even though wool production in 2014/15 is predicted to be the same as in 2013/14, the higher auction prices have flushed wool onto the market. The Australian Wool Exchange (AWEX) reports that the weight of auction offerings to 5 June were up by 8%, while the Australian Wool Testing Authority (AWTA) reports a 1.9% increase in the volume of wool tested for the season to May. This increased supply has come from stock held in broker’s stores and, to a lesser extent, from on-farm stocks held over from previous seasons.

While supplies are up in the short-term, it is likely that supply will fall in 2015/16. The Australian Wool Production Forecasting Committee predicts that Australian wool production will fall by 2.7% in 2015/16 due to a lower national sheep flock. This, plus a low carry-over of stocks in to the new season, will mean that auction supplies are likely to be tight in 2015/16, particularly in the first couple of months.

Outlook for the first half of 2015/16

It seems that conditions are right for a continued cyclical upturn in wool prices, at least for the first half of the 2015/16 season. Economic growth forecasts in the major advanced economies are for an improvement in 2015 and 2016. While economic growth is slowing in China as its economy undergoes a necessary structural change, it is still expected to grow at a solid rate of a little under 7% per year in 2015 and 2016.

Business conditions in the wool textile industry are expected to be good at least for the first six months of 2015/16. The woollen sector could reach a peak in the next few months, and as a result, demand for broader wools and Merino cardings pulls back from the current high levels. However, the worsted sector (which uses a longer length fleece wool to produce a smoother fabric such as men’s suits) seems set for a good period of growth, which should help Merino fleece wools. The expected lower supply levels will also help support prices.

Of course, there are risks to this positive outlook. The global economy remains volatile and fragile, which could spell danger. For example, certain economies in Europe could still turn for the worse, which could put pressure on retail sales and orders through the wool textile pipeline, ultimately affecting raw wool demand.

A second issue is that of prices of competing fibres. These are relatively subdued and have not experienced much of an increase in the past six months. This is in contrast to 2011 when prices for all textile fibres surged, driven higher by a spike in cotton prices due to short-term shortages. Now, cotton stocks are at exceedingly high levels, holding back prices for both cotton and synthetic fibre. This could in turn dampen the extent of price increases for wool in US$.

Producers would also be well aware that there can be a correction following the kind of price surge we have seen in the past few weeks. This has happened in the past and is likely to happen again.

Longer term drivers for the wool industry

While the prospects over the next six months are relatively bright, what about in the longer term?

Based on my own analysis and assessment, the longer-term prospects for demand for Australian wool will hinge mostly on global economic conditions and consumer income growth. Less important will be the relative production volumes and prices of competing fibres such as cotton, polyester staple fibre, acrylic fibre and viscose fibre. Australian and world wool production volumes are unlikely to increase much, if at all. Meanwhile, world production of chemical and man-made fibres will continue to grow. Therefore, wool cannot compete on price. It must compete on value and the fibre qualities.

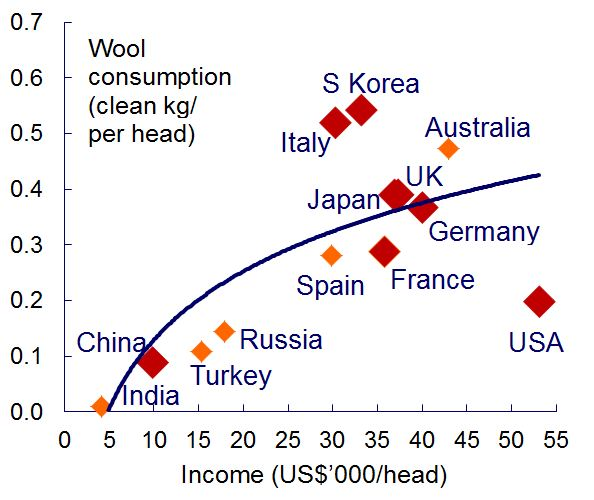

This will mean that wool clothing will appeal most to higher income consumers. As shown in Figure 3, there is a strong relationship between per capita income and the per capita consumption of apparel wool. The seven largest wool consuming countries in retail are shown by the large red markers. Wool consumption per capita in Australia is high, but with a relatively small population, total wool consumption in Australia is well below that of the seven largest consuming countries. The opportunities for growth in demand for wool are typified by the potential for per capita growth in China, Russia, India and Turkey.

With incomes being the most important driver, the key to growing demand will be products which meet consumer requirements and clothing trends. Worsted men’s suits, jackets and trousers, together with wool knitwear and women’s overcoats, will remain the backbone of demand for Australian wool. While there are likely to be fashion-driven fluctuations from year to year in the importance of these, as there currently is for women’s coats, the potential for longer-term growth in demand for wool will come from increased demand for active leisurewear (next-to-skin wear) and casual garments.

These product categories (both the traditional backbone categories and the potential growth categories) will determine the type of wool that will be demanded. It is therefore important for producers to understand the raw wool requirements that are used in each of these product categories.

While there will be sustained demand for wool in the longer-term, producers cannot simply rely on the hope that wool prices will increase. As indicated in the earlier discussion about the drivers in the current market environment, there are many external factors that influence wool prices and so prices will fluctuate. Producers should therefore develop a long-term strategy for their business that addresses the long-term opportunities that will be available and secures their long-term profitability.

Chris Wilcox is a key speaker at DAFWA’s Regional Sheep Updates on 28, 29 and 30 July 2015 and will cover this topic in more detail.

Sheep Updates is on again

The Department of Agriculture and Food, Western Australia (DAFWA), along with local grower groups and Making More From Sheep, invite you to join us at Regional Sheep Updates 2015. Industry leaders will detail the latest research, issues and trends, and explore the exciting future ahead for the Western Australian sheep meat and wool industries.

Highlights include:

- The short and long term future of wool – Chris Wilcox, Poimena Analysis

- How to economically finish your lambs: to feedlot or not? – Lucy Anderton, DAFWA

- Lifetime ewe management and boosting your lamb survival – Joe Young and Katherine Davies, DAFWA

- Optimising pastures to maximise your profit – Paul Sanford, DAFWA

- Sheep welfare – Lynne Bradshaw, RSPCA

- Anameka and other shrubs to fill feed gaps – Hayley Norman, CSIRO

- Using genomic technology to increase genetic gain – Stephen Lee, Sheep Cooperative Research Centre (Sheep CRC) & Adelaide University, and Dawson Bradford, Hillcroft Farms

- State of the Western Australian sheep flock – Kimbal Curtis and Kate Pritchett, DAFWA

- Optimising pastures at the farm scale to maximise profit – Paul Sanford, DAFWA

- Latest research and development on the transition from mulesing – Geoff Lindon, Australian Wool Innovation (AWI)

- Labour supply and training in the sheep industry, and opportunities and challenges facing youth in the sheep industry – Jackie Jarvis, Chamber of Commerce and Industry and Ben Patrick, 2014 Peter Westblade scholar.

| Location | Date | Local contact for registrations |

|---|---|---|

| Moora | Monday 27 July | Katherine Davies, DAFWA |

| Merredin Regional and Community Leisure Centre | Tuesday 28 July | Katherine Davies, DAFWA |

| Katanning Leisure Centre | Wednesday 29 July | Pip Crook, Southern Dirt Phone: +61 (0)8 9831 1074 Email: admin@southerndirt.com.au |

| Ravensthorpe Entertainment Centre | Thursday 30 July | Elisa Spengler, Ravensthorpe Agricultural Initiative Network Phone: +61 (0)41 717 4299 Email: rainoffice@westnet.com.au |

Registrations are open now! Visit our Sheep Updates webpage or speak to your local contact. A detailed agenda will be available on the webpage soon.

Sheep Updates are made possible through the Royalties for Regions $10 million Sheep Industry Business Innovation project, together with these partners:

Sheep producer survey sheds light on changes in Western Australia’s flock

Anne Jones

Department of Agriculture and Food, Western Australia – Albany

Email: Anne.Jones@agric.wa.gov.au

Early in 2011 and 2014 the Department of Agriculture and Food Western Australia (DAFWA) conducted surveys of sheep producers in which they were asked about their production systems, attitudes and behaviours to ewe and lamb management practices, breeding strategies and parasite control. The surveys were conducted as part of a national program undertaken on behalf of the Sheep Cooperative Research Centre.

Survey participants had more than 500 sheep and farmed in the medium rainfall zone or cereal-sheep zone. The 2011 and 2014 surveys attracted responses from about 380 Western Australian (WA) sheep producers.

The information gathered from the 2014 survey is currently being analysed and compared with the 2011 data. This paper presents the results on flock size and breeding strategy.

Primary enterprise type and production

Respondents were asked to identify their production type in three ways:

- Enterprise type (as wool production, prime lamb production or wool production and prime lamb production).

- Mating type (proportion of ewe flock mated as Merino (Merino ewes x Merino rams), terminal (Merino ewes x meat or maternal rams), and meat (meat or maternal ewes x meat or maternal rams).

- Ram selection strategy (either buy rams, breed rams for your own commercial flock, breed rams for sale or do not require rams).

Some general observations from the survey data were as follows:

- Dual enterprise systems are the most common in WA (at 56%), followed by wool (33%) and then prime lamb (12%) systems.

- The medium rainfall zone has a greater focus on prime lamb production than the cereal-sheep zone (16% versus 9%) and the cereal-sheep zone has a greater focus on wool production (35% versus 29%).

- Between 2011 and 2014 there has been a shift in the cereal-sheep zone back to wool production (up 7% to 35%) by wool and prime lamb producers.

- The average ewe flock size is larger in the medium rainfall zone than the cereal-sheep zone for both wool production (2240 versus 1671 ewes) and meat production (1367 versus 1042 ewes).

Proportion of mating types

Table 1 shows that while the dominant mating type for each enterprise reflects the enterprise type (e.g. 88% of all wool enterprise ewes mated were Merino ewes to Merino rams) other mating types play a considerable role in the make-up of any one enterprise. Twenty one percent of prime lamb producers have more than 33% of their ewe flock mated to Merinos. There were 8% of all respondents that mated no Merino ewes. The 2011 survey revealed similar results.

| Enterprise type | Number (No) | Merino | Mixed | Meat |

|---|---|---|---|---|

| Wool | 123 | 88% | 11% | 2% |

| Prime lamb | 44 | 9% | 12% | 79% |

| Wool and prime lamb | 210 | 45% | 36% | 18% |

Ram source

The majority of producers buy some rams to service their flock (69%, down from 76% in 2011). Fourteen per cent of respondents can be classified as ‘ram sellers’. As an additional 24% also breed rams for themselves, this gives a total of 38% of producers that breed rams either for themselves or for sale. This has not significantly changed since 2011.

Lamb producers are much more likely to breed rams for sale than other enterprises (30%). This is consistent with the data collected in 2011. The only notable change between years is that the proportion of wool producers that breed rams for their own flock has increased from 28% of wool producers in 2011 to 42% of wool producers in 2014.

| Enterprise type | No | Buy rams | Breed rams for self | Breed rams for sale | Don't breed |

|---|---|---|---|---|---|

| Wool | 123 | 67% | 42% | 15%b | 3% |

| Prime lamb | 44 | 61% | 34% | 30%a | 2% |

| Wool and prime lamb | 210 | 71% | 31% | 10%b | 8% |

| WA | 377 | 69% | 35% | 14% | 6% |

Stud selection

Respondents that buy in rams were asked how they usually select their ram source and their rams. The options provided for how they chose their ram source were:

- I have never considered going to anyone other than my regular stud breeder

- I choose a stud breeder based on advice from my classer, agent or consultant

- I usually go to the ram sales or shows and select a stud that suits my needs

- I review wether trial data, sire evaluation data, sale reports etc. and select a stud breeder that is performing well

- I use Australian Sheep Breeding Values (ASBVs) or information from Sheep Genetics and/or selection indexes to select a breeder that matches my breeding objective.

Producers in the medium rainfall zone were more likely to use genetic information when selecting a ram source (26%) than producers in the cereal-sheep zone (15%). There are no significant differences between wool and prime lamb producers and prime lamb producers or wool producers; however there is a significant difference between lamb and wool enterprises in that wool producers are more likely to take the advice of a classer or agent when choosing a ram source.

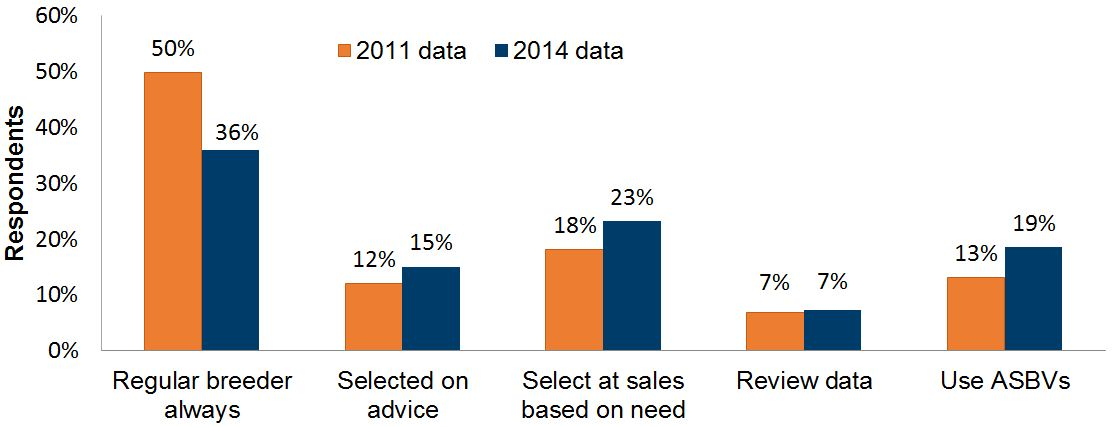

Comparing the responses from the 2011 and 2014 surveys (Figure 1) shows that there are far fewer producers choosing to select their rams from their regular breeders (36% in 2014 compared to 50% in 2011). All the other options have experienced slightly larger numbers of producers indicating a subtle shift toward more objective methods of ram stud selection.

Ram selection

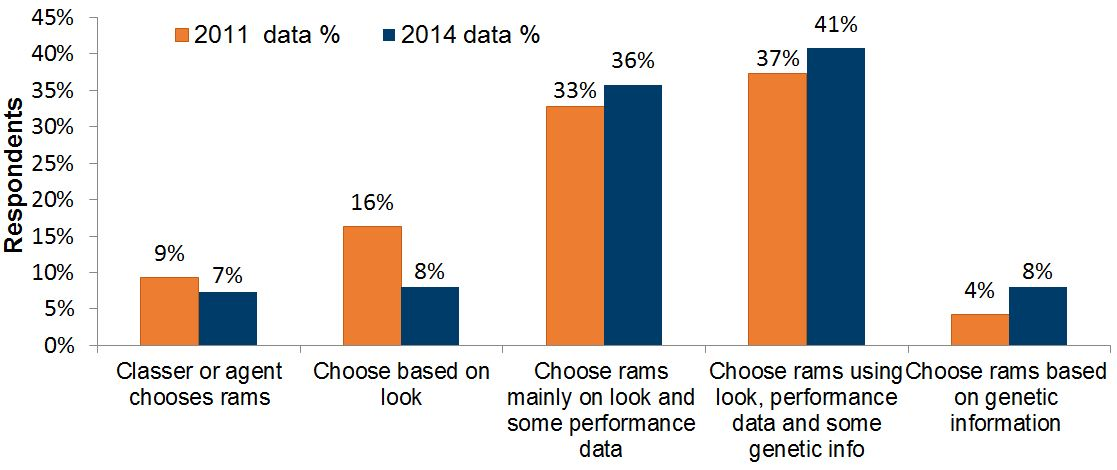

Most ram buyers chose their rams with some combination of how they look and some performance data (77%). Forty nine percent of producers use genetic information (either primarily or in combination with other methods) to select their rams. Between enterprise types, prime lamb enterprises are more inclined (19%) to select rams based on how they look than wool enterprises (6%). The 2014 results were not significantly different from the 2011 result.

Figure 2 shows that there has been a shift toward the use of performance data or genetic information. Since 2011, fewer producers are now saying that they select mainly on visual appeal (8% in 2014 compared to 16% in 2011). In 2011, 74% of producers selected rams based on some level of performance data or genetic information, while in 2014, 85% of producers that bought rams used performance data or genetic information to some degree.

Knowledge and use of Australian Sheep Breeding Values

The 2014 producer survey included the question “Which one of the following statements best describes your current level of knowledge of Australian Sheep Breeding Values (ASBVs)?” The options for response were:

- I have never heard of ASBVs

- I have heard of ASBVs but don’t understand them

- I have a basic understanding of ASBVs

- I have a good understanding of ASBVs

- I have a detailed knowledge of ASBVs.

There was no difference in understanding of ASBVs between producers in different zones. In comparing enterprise type, however, a much larger proportion of prime lamb producers claimed to have a detailed knowledge of ASBVs (14%) compared to other enterprise types (4%).

More WA producers had not heard of ASBVs compared to the national average (13% of WA producers compared to 8% nationally) and fewer WA producers consider themselves to have a detailed knowledge of ASBVs (4% compared to 9% nationally). Refer Figure 3.

Use of ASBVs in ram marketing

Two further questions were asked of the 53 ram sellers: “How many rams did you sell in 2013?” and “What percentage of the rams that you sold (or sold semen from) in 2013 had ASBVs?” Six ram sellers sold a portion of their rams with ASBVs. All other ram sellers either sold all or none of their stock with ASBVs. Table 3 summarises the data associated with the ‘all’ or ‘none’ groups of breeders.

| Parameter | 2011 No | 2011 % | 2014 No | 2014 % |

|---|---|---|---|---|

| No. ram sellers with 100% ASBVs | 14 | 33% | 17 | 36% |

| No. ram sellers with no ASBVs | 28 | 67% | 30 | 64% |

| Average no. rams with ASBVs | 180 | — | 141 | — |

| Average no. rams with no ASBVs | 97 | — | 80 | — |

| Total no. rams with ASBVs | 2520 | 48% | 2396 | 50% |

| Total no. rams with no ASBVs | 2710 | 52% | 2395 | 50% |

Forty nine percent of all rams sold by the WA survey respondents were sold with ASBVs. There has been a considerable decline in the total number of rams sold by ram sellers. This information, in conjunction with the data on breeding strategies, indicates that there has been a real decrease in the demand for rams by commercial producers that has impacted on the turnover and income of ram breeders.

A second article covering the survey results on the management of ewe flocks and reproduction rates will be in the next edition of Ovine Observer.

Infertility and abortion in ewes

Anna Erickson

Department of Agriculture and Food, Western Australia – Narrogin

Email: anna.erickson@agric.wa.gov.au

DAFWA’s Animal Health Labs investigate infertility or abortion in sheep every year. There are multiple possible causes of both infertility and abortion, but making a definitive diagnosis is often very difficult. This is for several reasons:

- Testing is often retrospective. Diagnosis of infertility is often only made at scanning while the cause of the problem was earlier, at joining. Similarly, investigation of foetal loss, abortion or early lamb deaths may only be instigated at marking.

- Incomplete sample sets are often submitted. For extensive testing a wide set of samples is required. This includes blood from both the ewe and her flock mates, vaginal swabs, and samples from the placenta and aborted foetus. These last two are often not available.

- A number of non-infectious factors can cause infertility including nutrition, trace element deficiencies, management problems and severe weather events.

It is important to distinguish between infertility and abortion. Causes of infertility (failure to conceive) include ram and ewe factors. Selected issues are discussed below.

Ram factors:

- Brucella ovis infection results in epididymitis and reduced sperm production. Producers should buy rams only from B.ovis accredited flocks, and run young rams separately from older or suspect rams in the off season. Maintain good boundary fences to keep out strays. Check all rams for any signs of testicular and epididymal disease before joining and cull any suspect animals.

- Testicular inflammation. Several infections including Corynebacterium pseudotuberculosis (cheesy gland), Actinobacillus seminis and Histophilus somni can cause abscesses or inflammation that decrease sperm production. Rams should be vaccinated against cheesy gland and checked for testicular disease (see B.ovis above).

- Any condition which causes a fever or rise in body temperature can damage sperm. As sperm production takes at least six weeks, infertility will continue until maturation of new healthy sperm. Temporary infertility can result from:

- Shearing – increased susceptibility to heat stress during the summer, as well as infection of shearing cuts.

- Dipping – apart from infection, dips may produce fever for a short period.

- Droving – fast droving in hot weather can cause a significant rise in body temperature. Many breeders prefer to deliver the rams to the joining paddock by truck.

- Flystrike – flystrike is invariably associated with fever. It is good practice to jet the polls of rams prior to joining.

- Over-fat rams – over conditioned rams are more likely to be affected by hot weather and droving, and can get a high temperature when going straight into work.

- Some drugs can suppress sperm production. Always check with a vet before giving medications.

All management procedures such as shearing and dipping should be done well ahead of joining. The six week sperm production period should also be considered in other aspects of pre-joining ram management, including for supplementary feeding and examination.

Ewe factors:

- Brucella ovis. Ewes infected with B.ovis at mating usually abort at a very early stage and return to oestrus. They are a source of the infection for rams during this time. Most ewes will not remain infected for more than two oestrus cycles but this can cause a prolonged lambing period. For those using a very short joining period it can result in very low pregnancy rates.

- Clover disease. Sheep grazing pastures with more than 30% of Trifolium species clovers early in the growing season may show reduced conception rates. Mature pastures are less risky.

- Ewe condition. Ewe condition at joining is strongly linked to flock fertility, ewe condition at lambing and lamb and dam survival. Greater than 85% of the ewe flock should be in BCS 3 or higher at joining to maximise flock fertility.

Abortion is defined as the termination of a pregnancy. It is normal for 1.5–2% of ewes to abort in any one year, but abortion ‘storms’ with rates above 5% should be investigated. These can occur at any stage of the pregnancy but later term abortions are more often noticed. Even in later abortions, scavengers will often remove the foetus and afterbirth before producers notice it, so an issue with abortions may only be diagnosed retrospectively. Monitoring of the flock for evidence of abortion allows early detection and the best chance of obtaining diagnostic samples. A firm diagnosis allows implementation of the most cost effective intervention and best advice on avoiding the problem in subsequent seasons.

Infectious causes of abortion include:

- Toxoplasmosis. This causes late abortions and stillbirths. The source of the infection is feed or pastures contaminated by cysts and shed in the faeces of infected cats. There is no effective treatment. Control mainly consists of controlling feral and domestic cats’ access to sheds used to store sheep feed. During an outbreak, prompt removal of any aborted material may help reduce the extent of the outbreak.

- Listeriosis. This causes abortions five to six weeks before the expected date of lambing. It can also cause stillbirths and increased death rates in the first few days after birth. Abortion rates can be up to 20%. Some apparently healthy animals carry Listeria but the most common source of the infection is damp or spoiled feed, especially hay or poorly prepared silage.

- Campylobacter infection. This causes late abortions and weak or stillborn lambs. Campylobacter survives in the digestive system of some sheep and cattle and is shed onto pasture. Antibiotics may help reduce the extent of an abortion storm due to Campylobacter, along with hygiene and prompt removal of any aborted material. There is a vaccine available for Campylobacter in sheep which may be useful in protecting naïve flocks (flocks where the infection is not currently present, based on blood test results) or when introducing maiden ewes into a flock where infection is known to be present. However, independent advice should always be sought from a veterinary surgeon before starting a vaccination programme.

- Other infectious causes of ewe abortion include Q fever (Coxiella burnetti), leptospirosis, opportunistic bacterial infections and the Akabane and Border disease viruses.

- Non-infectious causes of abortion may include ergotism, metabolic disorders and nutritional deficiencies.

Several of the above infections are zoonoses, that is, they can cause disease in people. All producers should exercise extra hygiene when handling ewes that have aborted or the aborted material itself, including wearing gloves and washing hands and tools in soap or detergent. Toxoplasmosis and listeriosis are particularly a concern for pregnant women. Pregnant women should avoid handling aborting ewes until a diagnosis is made.

Enzootic abortion of ewes, caused by Chlamydophilia abortus, is exotic to Australia. This infection causes abortions, systemic illness with fever, and stillbirths. It is also a zoonosis. It is important to our export markets to be able to demonstrate continued freedom from enzootic abortion and therefore abortion storms in sheep should always be investigated.

Recently, sheep exports were disrupted by blood samples testing positive for Chlamydophilia abortus. These appear to be false positives, but sheep which test positive are excluded from export consignments. The exact reason for false positives is not clear but there may be cross reactions occurring with another strain of the bacteria, C pecorum, which is present in Australia and can cause pink eye, arthritis and pneumonia.

Producers with infertility or abortion should:

- undertake a thorough investigation of all likely causes before trusting one intervention to solve the issue

- consider other recommendations for maximising lambing percentage (Lifetime Wool/MLA – flock size, lambing condition, nutrition, shelter).

If you notice abortions in your sheep, or find your stock unexpectedly sick or dead, the Subsidised Disease Investigation Pilot Program can help you get the issue fully investigated by a veterinarian at reduced cost. The pilot program, funded by Royalties for Regions, subsidises the cost of full investigations into stock deaths or disease to increase surveillance and testing for exotic animal diseases in WA.

This testing supports the WA livestock industry but the added benefit is that, for reduced cost, you can find out the cause of the disease on your farm. This gives you the opportunity to put control measures in place to minimise losses. Contact your private or DAFWA veterinarian to request a subsidised disease investigation.

Ovine Johne's disease vaccination could help protect your sheep enterprise

Anna Erickson

Department of Agriculture and Food, Western Australia – Narrogin

Email: anna.erickson@agric.wa.gov.au

Producers should consider vaccinating this year's lambs against ovine Johne's disease at lamb marking time.

The prevalence of ovine Johne's disease (OJD) in Western Australia continues to increase, with some south western shires now having a flock prevalence of over 10%.

The disease is less common in the wheatbelt, but does occur.

There are documented cases in WA of death rates of 5-10% per annum due to the disease and clinical signs have been seen in animals as young as two years old.

When deciding whether to vaccinate or not you need to ask yourself two questions:

- What is the risk of OJD getting onto my property?

- Are there neighbouring properties with OJD?

- Are you at the bottom of a water catchment?

- Do you trade a lot of sheep?

- Are you in a high rainfall zone?

All of these factors increase the risk of OJD entering your property.

- If OJD does get onto my property, what is the impact of the diagnosis going to be?

- Are you a stud breeder?

- Do you sell sheep interstate?

- Are you in a high rainfall zone?

All of these factors mean that if you are diagnosed with OJD, the impact on your business is likely to be significant. The impact could be either immediately for stud breeders or those with an interstate market, or in the medium term for people farming in the high rainfall zone where the disease finds it easier to establish and spread.

Alternatively if you are (for example) primarily a buyer of lambs for feedlotting, although you are at risk of buying sheep which have been exposed to OJD, the sheep will have been sold to abattoir before any clinical signs develop.

OJD vaccine should be given before the lambs reach 16 weeks of age.

Lambs vaccinated at this age are 'approved vaccinates'.

They are considered to be at low risk of becoming infected with OJD and shedding the bacteria.

Only one vaccination is given – there is no need for annual boosters, and older animals can also be vaccinated if on-property tests show that the disease is not yet present on the property.

Vaccination remains the most effective way to control the disease on infected properties, however, vaccination alone should not be relied on to prevent OJD entering your property.

This is because the vaccination improves sheep immune response to an OJD challenge but like many vaccinations it is not 100% effective. This leaves a small chance that some animals can still become infected with OJD if they are on heavily contaminated paddocks.

However, if OJD does enter a property where the flock is vaccinated, the rate of clinical disease will be negligible provided vaccination cover is maintained.

For further information refer to the Ovine Johne's disease vaccination page on the Department of Agriculture and Food, Western Australia (DAFWA) website.

OJD has a very long incubation period, so if vaccination does not start until the disease is well established, it will take several years for vaccination to start to reduce death rates from the infection.

Producers who are not currently vaccinating should use the abattoir monitoring scheme to make regular checks on the OJD status of their flock as this allows vaccination to be started if and when the disease does get onto your property.

For information on the abattoir monitoring scheme, visit the ovine Johne's disease and abattoir inspections in WA page on the DAFWA website.

For more information contact Anna Erickson, Veterinary Officer, Narrogin on +61 (0)8 9881 0211.